20 Common Tax Mistakes That Could Cost You Thousands

Avoid these costly tax mistakes to keep more money in your pocket and prevent unnecessary penalties or audits.

- Chris Graciano

- 4 min read

Every year, taxpayers make avoidable mistakes. These errors can lead to overpayments, missed refunds, or IRS scrutiny. In this listicle, we highlight 20 common tax blunders and how to steer clear of them to maximize your financial return. From overlooking valuable deductions to simple filing errors, these missteps can result in losing thousands of dollars.

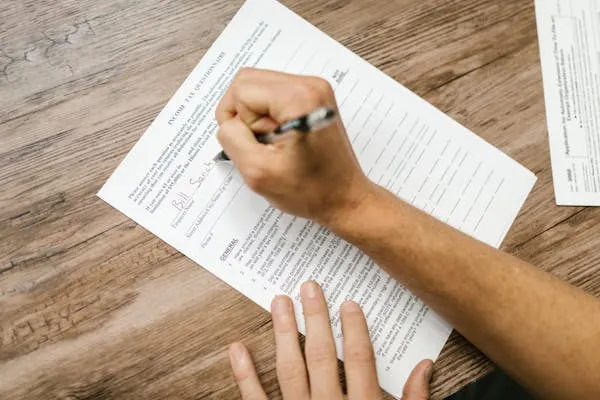

1. Filing Too Late

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Delaying your tax return can lead to penalties and interest on unpaid taxes. Even if you’re owed a refund, procrastination could mean missing the deadline altogether.

2. Incorrectly Entering Personal Information

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

A simple typo in your name, Social Security number, or bank details can delay processing. Mismatched information may trigger an IRS review, slowing down your refund.

3. Claiming the Wrong Filing Status

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Choosing the incorrect filing status can mean missing out on valuable credits or deductions. Many taxpayers mistakenly select “Single” instead of “Head of Household,” losing significant tax breaks.

4. Overlooking Earned Income Tax Credit (EITC)

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Millions of eligible taxpayers fail to claim this credit, missing out on thousands in refunds. It’s designed for low to moderate-income earners, and even some without children qualify.

5. Misreporting Income

Kindel Media on Pexels

Kindel Media on Pexels

Failing to report all taxable income, including freelance work or side gigs, can lead to IRS penalties. Employers and payment platforms send copies of earnings reports to the IRS, so discrepancies can raise red flags.

6. Forgetting to Sign Your Return

RDNE Stock project on Pexels

RDNE Stock project on Pexels

An unsigned tax return is invalid and won’t be processed. Paper filers often overlook this step, leading to delays or penalties.

7. Not Keeping Proper Documentation

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Receipts, invoices, and tax forms should be kept for several years in case of an audit. Without proof of deductions or expenses, the IRS can disallow claims, increasing your tax bill.

8. Ignoring State Taxes

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Some taxpayers focus solely on federal taxes and forget about state obligations. Missing state deadlines can result in unexpected bills, interest, and penalties.

9. Taking Ineligible Deductions

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Claiming deductions you don’t qualify for can trigger an audit or lead to fines. Common mistakes include overstating home office expenses or medical costs.

10. Failing to Report Cryptocurrency Transactions

Art Rachen on Unsplash

Art Rachen on Unsplash

The IRS treats cryptocurrency as taxable income, yet many forget to report trades or earnings. With increasing regulations, unreported crypto transactions can lead to audits and penalties.

11. Paying the Wrong Estimated Taxes (Self-Employed)

Windows on Unsplash

Windows on Unsplash

Freelancers and business owners must make quarterly estimated tax payments. Underpaying can result in penalties, while overpaying ties up cash unnecessarily.

12. Overlooking Education Tax Credits

Leeloo The First on Pexels

Leeloo The First on Pexels

Students and parents often forget about the American Opportunity and Lifetime Learning credits. These credits can significantly reduce tax liability, covering tuition, fees, and supplies.

13. Ignoring Required Minimum Distributions (RMDs)

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Retirees with traditional IRAs and 401(k)s must take minimum withdrawals annually. Skipping an RMD can lead to a hefty 50% penalty on the amount not withdrawn.

14. Incorrectly Calculating Home Office Deductions

Windows on Unsplash

Windows on Unsplash

Many taxpayers either overstate or underclaim home office expenses. The IRS has strict requirements, and claiming excessive deductions can lead to audits.

15. Forgetting to Update Withholding Amounts

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Failing to adjust your W-4 form after significant life events like marriage or having children can lead to unexpected tax bills. Too little withholding means you’ll owe money at tax time, while too much means smaller paychecks throughout the year.

16. Not Claiming Dependent Care Expenses

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Working parents who pay for daycare or after-school programs often miss out on the Child and Dependent Care Credit. This credit can reduce tax liability by up to 35% of qualifying expenses.

17. Missing Charitable Contribution Rules

Polina Tankilevitch on Pexels

Polina Tankilevitch on Pexels

Donations to qualified charities can provide valuable tax deductions, but missing proper documentation can invalidate claims. Non-cash donations, such as clothing or household goods, must have a fair market value assessment.

18. Overpaying on Capital Gains Taxes

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Selling investments without considering tax strategies can lead to higher capital gains taxes. Holding assets for more than a year qualifies for lower long-term rates.

19. Forgetting to Claim Health Insurance Premium Tax Credits

Leeloo The First on Pexels

Leeloo The First on Pexels

Taxpayers who purchase health insurance through the Marketplace may qualify for premium tax credits. Failing to claim this benefit means overpaying for coverage.

20. Not Seeking Professional Help When Needed

Mikhail Nilov on Pexels

Mikhail Nilov on Pexels

DIY tax filing can be cost-effective, but complex situations may require an expert. Overlooking deductions, misfiling, or misunderstanding tax laws can cost more than hiring a professional.