20 Simple Strategies to Lower Your Tax Bill

Tackle tax season with smart strategies to minimize your bill and maximize your savings.

- Daisy Montero

- 5 min read

Taking control of your taxes can make the process feel much easier. You can lower your tax bill by knowing which strategies actually work, like maximizing deductions, using tax credits, and planning smarter throughout the year. These ideas are practical, easy to follow, and can help you keep more of your hard-earned money. Let’s make filing of taxes less stressful and more rewarding.

1. Boost Your Retirement Savings and Lower Taxes

Andrea Piacquadio on Pexels

Andrea Piacquadio on Pexels

Contributing more to your 401(k) or IRA can lower your taxable income while building your nest egg for the future. These accounts offer tax benefits today, helping you save more long-term. Think ahead and take full advantage of these opportunities to save.

2. Don’t Miss Out on Tax Credits You’re Eligible For

Mikhail Nilov on Pexels

Mikhail Nilov on Pexels

Tax credits, like the Child Tax Credit or Earned Income Tax Credit, can reduce your tax bill dollar for dollar. If you’re eligible, these credits are a game changer, so make sure to claim them. They’re one of the easiest ways to save big on your taxes.

3. Make the Most of Your Charitable Giving

Tima Miroshnichenko on Pexels

Tima Miroshnichenko on Pexels

Donations to charities are tax-deductible, but you need to keep good records. Whether it’s cash or goods, giving to those in need can help you save on taxes. It’s a win for your tax bill and a win for causes you care about.

4. Maximize the Benefits of Your Health Savings Account (HSA)

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

An HSA gives you triple tax benefits; your contributions are tax-deductible, the account grows tax-free, and withdrawals for medical expenses are also tax-free. It’s a smart way to lower your taxes while saving for future healthcare needs.

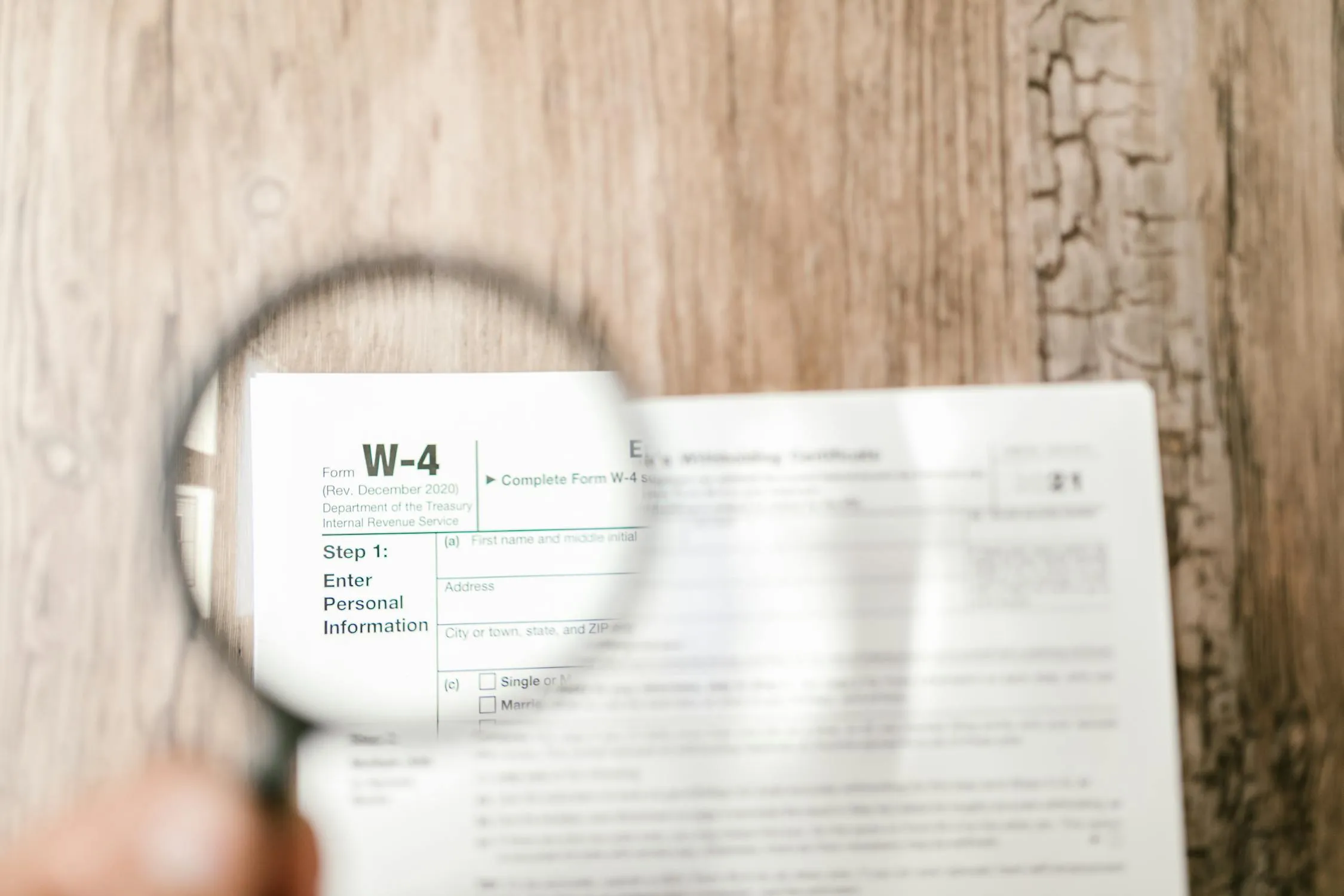

5. Update Your W-4 to Get Your Taxes Right

RDNE Stock project on Pexels

RDNE Stock project on Pexels

Adjusting your W-4 form ensures that the right amount of tax is withheld from your paycheck. Too much withheld means a larger refund, but too little could lead to a tax bill later. Check it every year to stay on track.

6. Claim All Your Self-Employment Expenses

Photo By: Kaboompics.com on Pexels

Photo By: Kaboompics.com on Pexels

If you’re self-employed, you can deduct business expenses like office supplies, travel, and even your phone bill. Keep detailed records and receipts so you don’t miss out on deductions to help lower your taxes.

7. Save on Taxes by Going Green

Kindel Media on Pexels

Kindel Media on Pexels

Energy-efficient upgrades like solar panels or better insulation can earn you tax credits. Not only will you reduce your carbon footprint but also your tax bill, making it a smart investment for your wallet and the planet.

8. Bundle Your Medical Expenses for Bigger Savings

cottonbro studio on Pexels

cottonbro studio on Pexels

Medical expenses are only deductible if they exceed a certain percentage of your income. If possible, bunch your medical expenses into one year, so you can reach that threshold and get a bigger deduction.

9. Take Advantage of Flexible Spending Accounts (FSAs)

Anna Shvets on Pexels

Anna Shvets on Pexels

FSAs let you use pre-tax dollars for healthcare and dependent care expenses. Just be sure to use the funds before the year ends to avoid losing them. It’s an easy way to lower your taxable income and cover everyday costs.

10. Offset Gains by Selling Underperforming Investments

Thirdman on Pexels

Thirdman on Pexels

Selling investments that have lost value can help offset any capital gains you’ve earned. This strategy, known as tax loss harvesting, can reduce your taxable income and lower your tax bill.

11. Claim Home Office Deductions If You Work from Home

Antoni Shkraba on Pexels

Antoni Shkraba on Pexels

You may qualify for a home office deduction if you’re working from home. Whether using part of your home exclusively for business or working remotely, you can deduct expenses like utilities, internet, and office supplies.

12. Take Full Advantage of Education-Related Tax Breaks

Mikhail Nilov on Pexels

Mikhail Nilov on Pexels

Tax credits like the American Opportunity Credit or Lifetime Learning Credit can offset the cost of tuition. Whether pursuing higher education or helping a child, don’t forget to check for credits that make education more affordable.

13. Look Into Tax Benefits for Your Kids

Getty Images on Unsplash

Getty Images on Unsplash

Kids bring more than joy; they also come with tax breaks. You can claim deductions for childcare expenses or quality for credits like the Child Tax Credit. It’s one way to save a little extra during tax season.

14. Invest in Real Estate for Long-Term Tax Benefits

AS Photography on Pexels

AS Photography on Pexels

Real estate investments come with tax advantages, like depreciation and potential deductions for property expenses. If you’re considering buying property, it could greatly reduce your taxable income in the long run.

15. Plan for Your Taxes Throughout the Year

Nataliya Vaitkevich on Pexels

Nataliya Vaitkevich on Pexels

Smart tax planning isn’t just a year-end activity. Keep track of your finances throughout the year so you can adjust and take advantage of deductions and credits before the deadline hits. Regular planning helps keep your taxes in check.

16. Utilize State-Specific Tax Breaks

Polina Tankilevitch on Pexels

Polina Tankilevitch on Pexels

Many states offer tax incentives for things like energy-efficient upgrades, college savings, and local charity donations. Ensure you know any state-specific benefits to lower your overall tax burden.

17. Keep Track of Your Tax-Deductible Work Expenses

Photo By: Kaboompics.com on Pexels

Photo By: Kaboompics.com on Pexels

Job-related expenses, like uniforms, supplies, and travel, can be deducted from your taxable income. Keep detailed records of these expenses to ensure you’re not missing out on savings come tax season.

18. Look Into Tax-Advantaged Investments

Tima Miroshnichenko on Pexels

Tima Miroshnichenko on Pexels

Certain investments, like municipal bonds, offer tax-free interest. If you want to reduce your tax burden while still earning, these could be worth considering as part of your investment strategy.

19. Take Advantage of Tax Deferrals

Kampus Production on Pexels

Kampus Production on Pexels

Tax deferral options like 401(k) plans and other retirement accounts allow your money to grow tax-free until you withdraw it. These accounts can help reduce your taxable income today, setting you up for a more comfortable retirement.

20. Don’t Forget About State and Local Tax Deductions

Leeloo The First on Pexels

Leeloo The First on Pexels

State and local taxes (SALT) are deductible, but there are limits. If you live in a high-tax state, make sure to claim this deduction. It can help reduce your federal tax bill, especially if your state taxes are high.